.png)

Aerospace & Defense: Growth, Constraints and Opportunities

- Apr 5

- 6 min read

Updated: 4 days ago

On April 1, 2026, NASA launched Artemis II mission aboard the Space Launch System, sending four astronauts on a ten-day journey around the Moon before returning to Earth. The mission marks the first crewed flight beyond low-Earth orbit since Apollo 17 and signals renewed momentum in human space exploration.

The milestone also highlights the broader evolution of the aerospace industry. Today, space exploration is advancing alongside strong growth in commercial aviation, rising defense investment, and an increasingly active space economy.

Against this backdrop, the aerospace and defense (A&D) industry is entering a new phase of expansion characterized by strong demand, record revenues, and accelerating investment across aviation, defense, and space. In 2024, the world’s top 100 aerospace and defense companies generated approximately $922 billion in combined revenue, the highest level ever recorded for the sector. At the same time, the commercial aerospace market alone is projected to grow around 12% year-on-year in 2025, supported by a 25% increase in aircraft deliveries and resilient demand across airline operations and aftermarket services.

Yet the sector’s growth trajectory is increasingly shaped by structural imbalances. Demand for aircraft, defense systems, and space infrastructure continues to outpace production capacity, while supply chain fragility, workforce shortages, and rising raw-material costs limit the speed at which the industry can scale.

This article provides a high-level overview of the aerospace and defense market, examining current industry growth, demand trends across aviation and defense, key structural challenges, and the investment outlook shaping opportunities for startups and investors.

1. Industry Growth & Revenue Trends

The global aerospace and defense sector experienced a strong financial recovery in 2024. Across the top 100 A&D companies by revenue, the industry generated $922 billion, reflecting strong growth in both commercial aviation and defense programs. Commercial aviation demand rebounded rapidly as global travel recovered, while governments increased defense spending in response to rising geopolitical tensions.

However, revenue growth has not been matched by proportional increases in production output. Many aerospace manufacturers continue to face labor shortages, supply chain disruptions and shortages of specialized materials, which are preventing the industry from fully meeting demand. Aircraft backlogs continue to expand as manufacturers struggle to accelerate production.

Raw material inflation further complicates the operating environment. Prices for key aerospace metals have risen significantly in recent years. Titanium prices have increased roughly 90% since 2022, while tariffs on steel and aluminum in certain markets have reached 50%, increasing manufacturing costs and forcing companies to rethink global sourcing strategies.

As a result, many aerospace companies are prioritizing operational resilience, diversifying suppliers, investing in digital manufacturing tools and redesigning operating models to better absorb supply disruptions.

2. Demand Trends.

2.1 Commercial Aviation.

Commercial aviation remains the primary growth engine of the aerospace industry. Global air travel continues to expand, with passenger traffic expected to increase by approximately 5.8% in 2025, driven by rising middle-class travel demand and the continued recovery of international routes.

Airlines are responding by placing large aircraft orders to modernize fleets and improve fuel efficiency. However, manufacturers have struggled to scale production fast enough to meet this demand. The global commercial aircraft backlog has surpassed 14,000 units, representing nearly a decade of production at current manufacturing rates.

Aircraft deliveries are expected to reach approximately 1,390 units in 2025, reflecting a gradual production ramp-up by major manufacturers. Boeing has increased output of its narrow-body aircraft and achieved production rates of around 38 aircraft per month for the 737 MAX program, while Airbus is steadily expanding production of its A320 family aircraft and aims to reach 75 aircraft per month by 2027.

Despite these increases, delivery timelines remain extended, forcing airlines to keep aircraft in service longer than originally planned. This dynamic is fueling rapid growth in the aerospace aftermarket.

2.2 Aftermarket and MRO.

Within the broader aviation ecosystem, value is increasingly shifting toward the aftermarket as aircraft lifecycles are extended. Maintenance, repair, and overhaul (MRO) services have become one of the fastest-growing segments of the aerospace ecosystem. Global MRO spending is projected to grow approximately 14% year-on-year in 2025, driven by rising aircraft utilization and delayed fleet replacement cycles.

Aging fleets and extended aircraft service lives are creating sustained demand for engine maintenance, spare parts and repair services. In the first half of 2025, several major aerospace service providers recorded strong revenue growth, including Rolls-Royce, which reported roughly 28% revenue growth, and GE Aerospace, which grew around 23%over the same period.

However, the MRO sector is also facing capacity constraints. Skilled maintenance technicians remain in short supply, while parts shortages and logistical delays continue to slow repair turnaround times. To address these challenges, service providers are increasingly adopting AI-enabled predictive maintenance systems and digital diagnostics, allowing them to automate inspections, predict component failures and optimize maintenance schedules.

2.3 Defense Spending and Technology Investment.

Defense remains another major growth pillar for the aerospace industry. Global defense budgets increased by approximately 9% in 2024, reflecting rising geopolitical tensions and expanding investments in advanced technologies.

Governments are prioritizing capabilities in several strategic areas:

Cyber defense and digital warfare

Autonomous and unmanned systems

Missile defense and advanced air mobility

Space-based surveillance and communication systems

However, defense procurement cycles remain complex and uneven across regions. Programs often involve multi-year approval processes and varying national requirements, creating challenges for companies attempting to scale production across international markets.

For startups and investors, defense modernization programs are increasingly creating opportunities in dual-use technologies, where innovations developed for commercial aerospace, such as AI, autonomy and advanced sensors, can also be applied in military systems.

3. Space economy expansion.

The space sector continues to experience sustained investment growth, driven by both commercial innovation and national security priorities. Satellite communications, Earth observation systems and launch services are expanding rapidly as governments and private companies increase their presence in orbit.

Public and private capital flows into the space economy have grown consistently over the past decade, supporting the development of new satellite constellations, reusable launch vehicles and deep-space exploration programs. At the same time, space is becoming an increasingly strategic domain for defense and security operations.

The convergence of commercial and defense demand is accelerating innovation across the space ecosystem. However, regulatory frameworks, funding structures and infrastructure capabilities are still evolving, creating both uncertainty and opportunity for new entrants.

4. Operational and structural constraints.

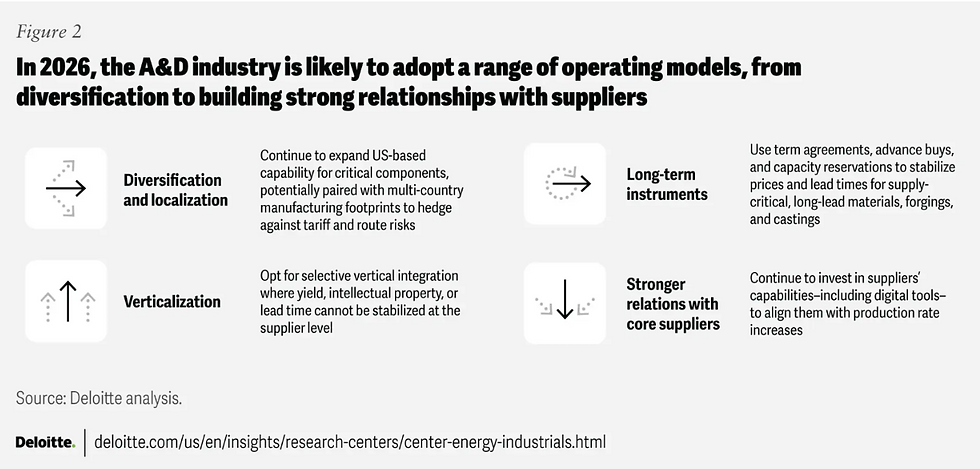

Supply chains remain a key structural challenge for the aerospace and defense (A&D) industry. Strong demand growth is occurring alongside shortages of raw materials, skilled labor, and ongoing geopolitical disruptions. Although supply conditions for some components have improved, constraints are expected to persist through at least 2027.

This creates a core tension for A&D companies: supply chains must become more efficient while also more resilient. Fragility across supplier networks now affects not only costs but also production schedules and delivery reliability. The pressure is likely to intensify as defense contractors increase output of missiles, munitions, and drones, while aircraft manufacturers push for higher production rates.

In response, companies are adjusting their strategies. Some U.S. firms are consolidating supply chains domestically to reduce uncertainty, while international partners are encouraging greater diversification beyond U.S.-centric suppliers. Many industry leaders are focusing on several key priorities:

Diversifying global supply ecosystems to reduce dependence on single-region sourcing

Deploying digital technologies such as AI, digital twins and predictive analytics to improve operational visibility

Reskilling the workforce to support increasingly automated and digital manufacturing systems

Redesigning operating models to improve flexibility and resilience

For startups and venture capital investors, these structural challenges represent a powerful opportunity. The aerospace industry remains capital-intensive and highly regulated, but the growing need for technology-driven solutions across manufacturing, maintenance, logistics and space infrastructure is opening new entry points for innovation.

5. Investment Outlook & Technology Opportunities.

While revenue across the aerospace sector has reached record levels, deal activity has remained relatively stable rather than sharply accelerating. Mergers and acquisitions in 2024 did not fully return to the peaks seen before the pandemic, though transaction volume remained consistent across several industry segments.

Instead of pursuing large consolidation deals, many companies are focusing on strategic acquisitions aimed at strengthening supply chains or enhancing digital capabilities. These targeted investments reflect a shift toward long-term operational transformation rather than short-term scale expansion.

For venture capital and startup ecosystems, the most active investment areas increasingly include:

Digital supply chain platforms

AI-driven predictive maintenance systems

Advanced manufacturing technologies

Autonomous aviation systems

Satellite infrastructure and space logistics

These technologies address some of the industry’s most persistent operational bottlenecks, making them particularly attractive to both strategic investors and venture funds. Looking ahead to 2026 and beyond, the aerospace and defense sector is expected to continue expanding, supported by strong global travel demand, rising defense budgets and sustained investment in the space economy.

References

Low, L. E. (2026, April 2). NASA. https://www.nasa.gov/news-release/nasas-artemis-ii-mission-leaves-earth-orbit-for-flight-around-moon/

Sample, I. (2026, April 1). The Guardian. https://www.theguardian.com/science/2026/apr/01/nasa-rocket-moon-launch-artemis-ii

PwC. (2024). https://www.pwc.com/us/en/industries/industrial-products/library/aerospace-defense-review-and-forecast.html

Accenture. (2025, October). https://www.accenture.com/content/dam/accenture/final/accenture-com/document-4/Accenture-Commercial-Aerospace-Insight-Report-October-2025.pdf